24/07/19 07:01

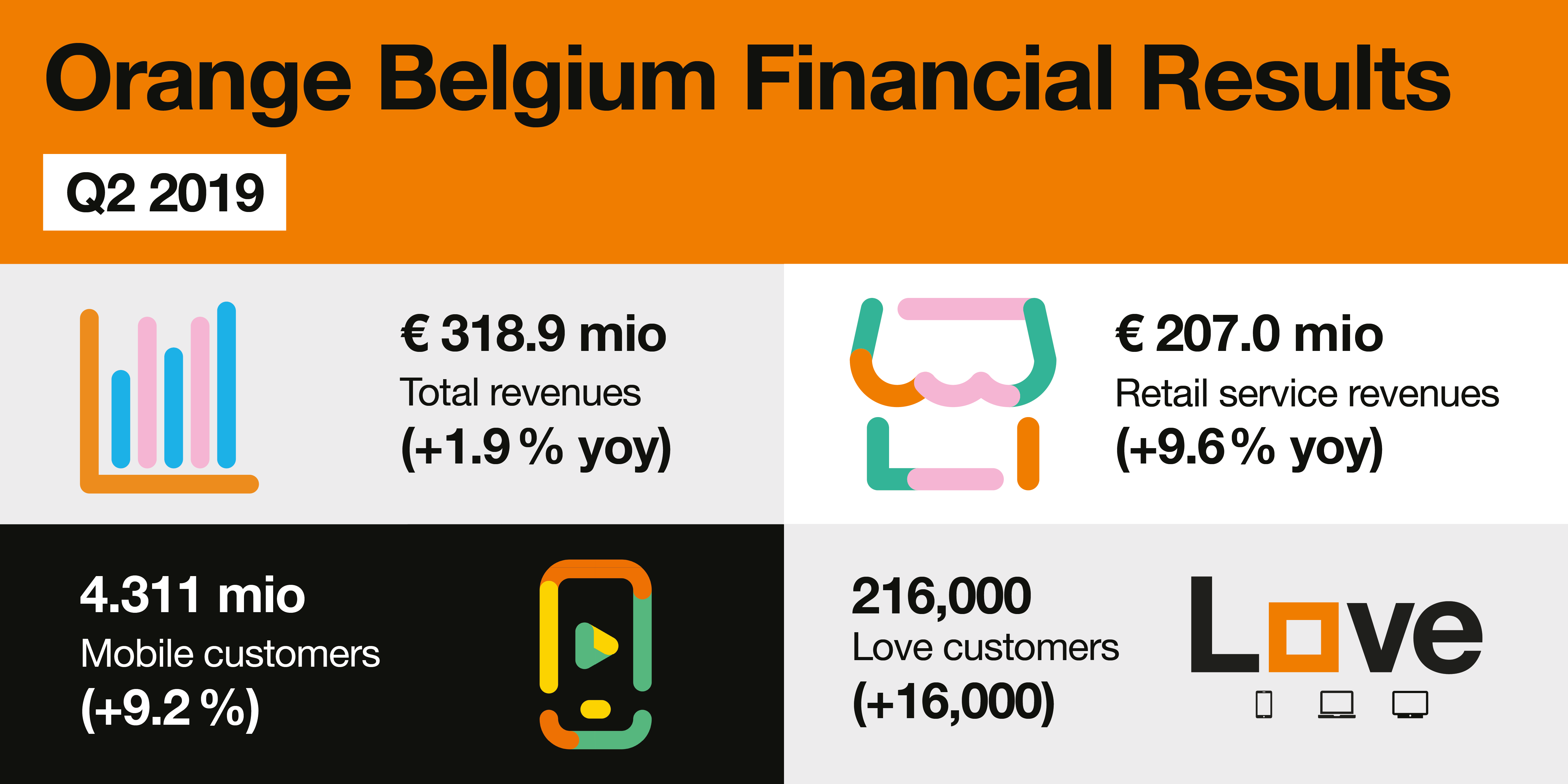

Financial information for the second quarter of 2019 and first half of 2019

4th consecutive quarter of near double-digit growth in retail service revenues

- Mobile postpaid customer base grew 6.8% yoy on quarterly net-adds of 26k

- Convergence customer base increased 58.8% yoy on quarterly net-adds of 16k

- Revenues: +1.9% yoy for the quarter / Retail service revenues:+9.6% yoy for the quarter

- EBITDAaL +18.2% yoy for the quarter (H1’19 : +7.4% yoy, +4.2% excluding seasonality effect)

Belgium Q2’19 operating highlights

- Bold challenger positioning is driving operating and financial performance. Orange Belgium has been drilling consistent messages around delivering better value proposition, simple tariffs (generous data and voice allowance), no bad surprises and no price increases. That bold positioning is being increasingly anchored in the consumers’ brand perception.

- Mobile postpaid continues its growth trajectory. The mobile postpaid customer base grew 6.8% yoy to 2.5m with net-adds of 26k subscribers during the quarter. An increasing number of subscribers continue to opt for higher tariff plans

- 16k convergent net-adds. Orange Belgium reached 216k Love customers, just prior to the launch of Love Duo. The convergent mobile subscriber base represents 13.6% of mobile postpaid customers (Q1’19: 12.7%).

- Mobile only postpaid ARPO decreased by 3.2% yoy. Regulation on intra-EU calls as well as continuous migration towards simple abundant tariff plans continued to drive out-of-bundle revenues lower - in line with Orange Belgium’s commitment to “no bad surprises”. The decrease in out-of-bundle revenues was partially offset by growing access revenues. B2C convergent ARPO increased 4.1% yoy, driven by the absence of discounts, revenues from set-up fees and fixed line option.

Orange Belgium: key operating figures

|

|

Q2 2018 |

Q2 2019 |

change |

|

Mobile postpaid customer base (in ‘000) |

2,355 |

2,516 |

6.8% |

|

Net adds (in ‘000) |

26 |

26 |

1.1% |

|

Mobile only postpaid ARPO (€ per month) |

21.3 |

20.6 |

-3.2% |

|

Convergent customer base (in ‘000) |

136 |

216 |

58.8% |

|

Net adds (in ‘000) |

14 |

16 |

10.9% |

|

B2C convergent ARPO (€ per month) |

73.7 |

76.8 |

4.1% |

|

Convergent mobile customer as % mobile contract customer base |

8.8% |

13.6% |

481 bp |

|

|

|

|

|

Q2’19 consolidated financial highlights

- Revenues increased by 1.9% yoy to €318.9m thanks to sustained strong growth (+9.6%) in retail service revenues, offsetting lower MVNO revenues while Medialaan completed its migration towards Orange Belgium’s network in June.

- EBITDAaL increased by 18.2% yoy to €78.9m despite lower MVNO revenues. The drivers were: higher retail service revenues; cost control; cable operations improvement; and a €4m tailwind from the seasonality in advertising and IT spend.

- eCapex decreased 5.6% to €42.9m.

- Operating cash flow increased to €36.0m on improved profitability. Net financial debt amounted to €248.8m.

- Cable operations continue to improve. Cable generated a positive EBITDAaL of €1.3m in H1’19 thanks to continuous effort on operational efficiency. H1’19 cable operating cash flow remains negative (-€22.0m) on eCapex of €23.3m.

- 2019 financial guidance reiterated. Orange Belgium Group expects slight revenue growth, EBITDAaL of €285m-€305m and stable eCapex.

Orange Belgium Group: key financial figures

|

reported |

comparable |

|

comparable |

reported |

reported |

comparable |

|

comparable |

reported |

||

|

in €m |

Q2 2018 |

Q2 2018 |

Q2 2019 |

change |

change |

H1 2018 |

H1 2018 |

H1 2019 |

change |

change |

|

|

Revenues |

313.0 |

318.9 |

1.9% |

619.6 |

637.1 |

2.8% |

|||||

|

Retail service revenues |

188.8 |

207.0 |

9.6% |

370.0 |

412.6 |

11.5% |

|||||

|

|

|

|

|||||||||

|

EBITDAaL |

66.7 |

78.9 |

18.2% |

|

127.5 |

136.9 |

7.4% |

||||

|

margin as % of revenues |

21.3% |

24.7% |

342bp |

|

20.6% |

21.5% |

91 bp |

||||

|

eCapex |

-45.5 |

-42.9 |

-5.6% |

|

-77.3 |

-79.8 |

3.3% |

||||

|

Operating cash flow1 |

21.2 |

36.0 |

69.3% |

|

50.2 |

57.1 |

13.7% |

||||

|

|

|

|

|||||||||

|

Adjusted EBITDA |

66.7 |

|

127.3 |

|

|||||||

|

margin as % of revenues |

21.3% |

|

20.5% |

|

|||||||

|

Capex |

-45.5 |

|

-77.3 |

|

|||||||

|

Operating cash flow2 |

21.2 |

|

50.0 |

|

|||||||

|

|

|

|

|||||||||

|

Net financial debt |

305.1 |

248.8 |

305.1 |

248.8 |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

1 Operating cash flow defined as EBITDAaL – eCapex

2 Operating cash flow defined as Adjusted EBITDA –Capex

Michaël Trabbia, Chief Executive Officer, commented:

As a Bold challenger, we must remain true to our customer promise for simple, generous and worry-free tariffs. We are against bad surprises, be it unjustified price increases or unreasonable out-of-bundle fees. This quarter, we pushed this customer promise further by making MMS free of charge and by extending our unlimited data tariff plans for use throughout the EU.

This consistent positioning drove a significant change in Orange’s brand’s perception in Belgium. In an active competitive environment, this translated into steady commercial results, both on mobile and convergence as well as sustained strong retail service revenues growth.

Going one step further, we launched our long awaited Love Duo offer (mobile + unlimited broadband), designed for the cord-cutters who don’t want to be forced to pay for a service they don’t use.

Finally, the recently announced radio access network sharing agreement will help us improve network quality and accelerate 5G roll-out. This operational transaction will allow us to maintain our focus on real differentiation areas for our customers while preserving an effective competitive environment.

Arnaud Castille, Chief Financial Officer, stated:

The highlights of the second quarter were once again steady commercial and financial results. This demonstrates that our commercial focus on granting our clients simple and worry-free offers is bearing its fruits since we launched our unlimited offers last year.

I am pleased to report a fourth consecutive quarter of near double-digit growth in retail service revenues. The latter was mainly driven by convergent services as well as continued growth in our core mobile business. We continued to manage our operating expenses, thus growing EBITDAaL despite lower MVNO revenues.

We recently received the competition authority’s approval of the acquisition of BKM. We expect to finalize the transaction imminently. This acquisition will allow us to enhance our B2B offering and grow our presence in the ICT and connectivity markets.

We confirm our guidance for 2019. We are committed to delivering excellent customer service in order to maintain the commercial momentum. We remain extremely focused on extracting operational efficiencies.